Risk is everywhere during international transit. Whether you are shipping standard containers or multimillion-dollar oversized project cargo to Africa, understanding Cargo Insurance is not optional—it is a critical component of supply chain security.

What exactly does cargo insurance cover? How do you choose the right policy? What happens when a claim arises? In this comprehensive guide, SPEED INT'L breaks down everything you need to know about marine and freight insurance.

An insurance policy acts as a "risk map," detailing who is covered, what is covered, and the exclusions. A standard cargo insurance contract includes:

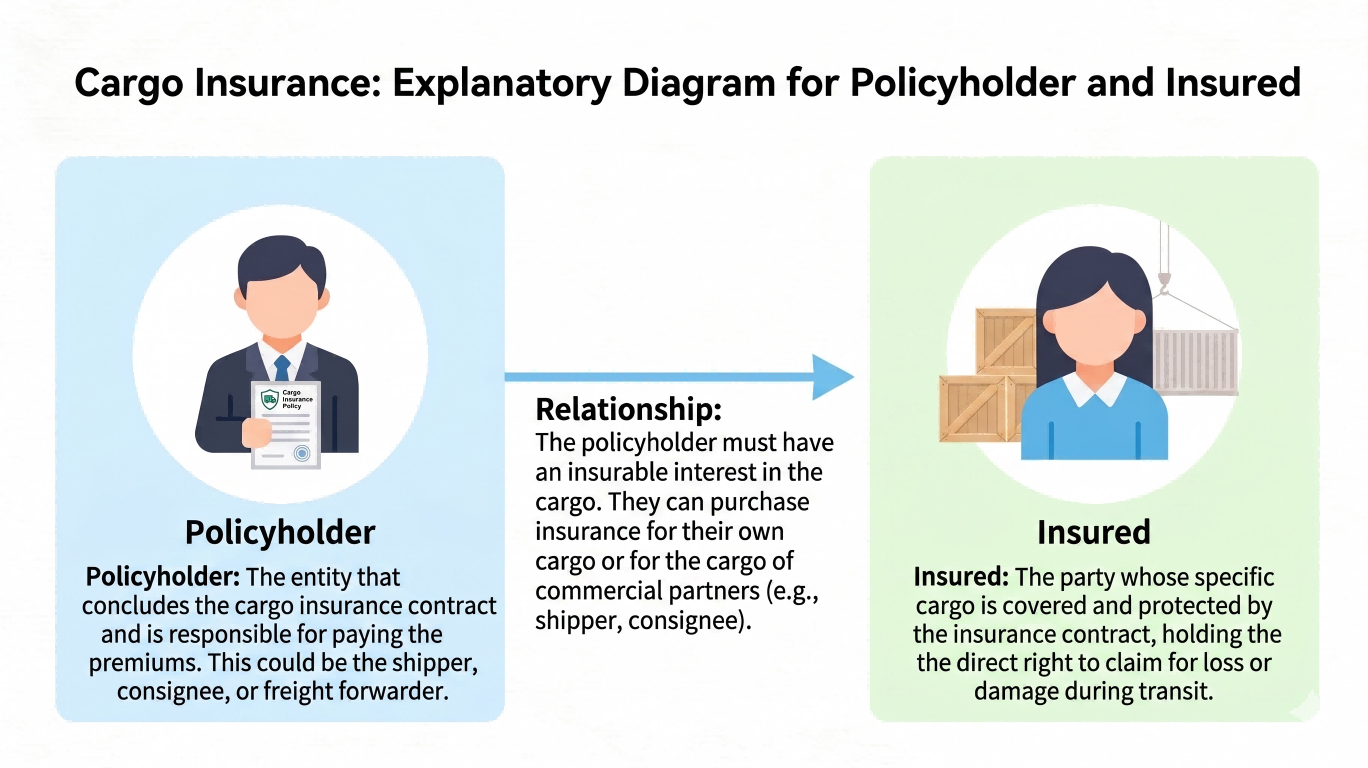

The Policyholder is the entity that signs the contract and pays the premium. The Insured is the entity whose financial interests are protected and holds the right to claim compensation after an accident.

In B2B cargo insurance, the Insured is typically the enterprise owning the cargo (the Shipper or Consignee). Note: Claim payouts are strictly made via corporate bank accounts, not to individuals.

Fig 1: The relationship between the Policyholder and the Insured.

The two most common international marine insurance clauses are:

Institute Cargo Clauses (A) - "All Risks":

Provides the broadest coverage. It covers all risks of loss or damage to the goods, minus specific exclusions. Ideal for most new, high-value commercial goods and project cargo.

Institute Cargo Clauses (C) - "Basic Risks":

Provides narrow, named-peril coverage (e.g., major disasters like fire, sinking, overturning). Often used for second-hand goods, raw materials, or specific inland transit legs.

The insured amount is the basis for premium calculation and the maximum payout.

If your cargo arrives damaged, taking the wrong steps can void your claim. Follow this protocol:

To expedite the claims process, prepare the following complete documentation:

Cargo insurance is not just another line item; it is an essential component of professional risk management. Understanding the fine print ensures your B2B bottom line is protected. As a certified NVOCC, SPEED INT'L offers expert guidance on securing your heavy lift and commercial shipments to Africa.

Get a Secure Shipping Quote